Acme United Stock Review

If you have school-age kids, you have seen their products but probably don’t know the company that makes them.

Today, we will review Acme United ACU 0.00%↑ in detail to determine whether it is attractive enough for our value portfolio.

In this review, we will cover:

A brief description of Acme United’s business

A detailed walkthrough of their financial strength and metrics

A rundown of the current business environment they are in, as well as the future outlook

Review the valuation of the ACU 0.00%↑ stock

Estimate the fair value of the stock, appreciation potential and determine whether the stock is a BUY or AVOID

So let’s get started.

All analysis below is done using data from Stock Rover (affiliate link). I have been using this software for 3 years now and it has taken hours off my investment research every week. There is nothing better for long term investors, if you invest in the US stock market (stocks or ETFs). Their highest level plan costs less than $1 per day, which is probably the best value available today in the stock market.

Acme United Company

Acme United is a leading supplier of cutting, measuring, and safety products for various markets, including school, home, office, hardware, and industrial. The company operates in the United States, Canada, Europe, and Asia. Acme United's nine main brands are Westcott, Clauss, PhysiciansCare, Pac-Kit, First Aid Only, Med-Nap, DMT, Spill Magic, and Safety Made.

A Brief History of Acme United

Acme United was founded in 1867 when German immigrant Leo Renz purchased a grist mill and opened Renz Shear Shop in Naugatuck, Connecticut. The company manufactured scissors and cast iron shears. In 1873, the business was incorporated as The Renz Shear Company.

In the 1880s, the company moved to Bridgeport, Connecticut, and was incorporated as The Acme Shear Company. The Wheeler brothers purchased the company, and their leadership led to its initial growth. Henry Wheeler, David C. Wheeler's grandson, became president in 1941 and continued to grow the company, which became the world's largest maker of shears and scissors by 1946. After World War II, Acme Shear established a subsidiary in the United Kingdom to sell directly to the European market. In 1965, the company began manufacturing disposable medical scissors and surgical instruments. A new plant was opened in Fremont, North Carolina to meet increased demand. Acme Shear went public in 1967.

Acquisitions and Name Change: In the 1970s, Acme Shear acquired Westcott Rule Company, a major ruler manufacturer founded in 1872. The company also acquired Acme Ruler & Advertising Co. in Canada. To reflect its expanded product line, the company's name was changed to Acme United Corporation.

Challenges and Restructuring: The 1980s presented challenges for Acme United as they became heavily dependent on one medical tools customer. When this customer began manufacturing its own products, Acme United lost over $20 million in annual sales. Acme United acquired several companies in the US and abroad in an attempt to survive, but these acquisitions met with varying levels of success. The company continued to experience losses in the early 1990s, resulting in pressure from shareholders to make management changes.

Turnaround and Renewed Growth: In 1995, Walter C. Johnsen was brought in as CEO. Under his leadership, a new management team was hired, the medical business was sold, and seven manufacturing plants were closed. By focusing on higher-margin products such as student scissors, rulers, and staplers, and expanding into the office market by selling to mass merchants, Acme United returned to profitability in 2000.

Strategic Acquisitions: Since its return to profitability, Acme United has pursued an aggressive growth strategy, focusing on acquiring companies that align with its core product categories. Some notable acquisitions include:

Clauss Cutlery in 2004

Camillus Cutlery Company in 2007

Pac-Kit Safety Equipment Company in 2011

The C-Thru Ruler Company in 2012

First Aid Only Inc. in 2014

Diamond Machining Technology (DMT) in 2016

Spill Magic Inc. in 2017

First Aid Central in 2020

Med-Nap LLC in 2020

Safety Made in 2022

Ready 4 Kits in 2022

Hawktree Solutions, Inc in 2023

Divestiture: In 2023, Acme United sold its Camillus and Cuda hunting and fishing product lines to GSM Holdings, Inc.

Acme United’s Financial Strength

What I really find interesting is the company’s refocusing on its core market and then expanding into adjacent markets strategically, and using acquisitions to grow into its markets. Many of the acquisitions were done at significant discounts to what could be considered the fair market value of the assets being acquired. The company has at many times chosen to acquire pieces of valuable assets (inventory, tooling, customer lists, accounts receivable, brand names, intellectual property, etc.) a-la-carte instead of buying the entire enterprise. Acquisitions by Assets is generally much cheaper than acquisitions by revenue (where you pay a multiple of Sales or EBITDA or something similar)

For example, in June 2013 they purchased certain assets of The C-Thru Ruler Company, a well-known supplier of drafting, measuring, lettering, and stencil products. Acme United purchased the inventory, tooling, brands, and other intellectual property for approximately $1.47 million. In 2011, C-Thru's revenues were about $2.5 million with gross profits reaching roughly $1 million. Since they already owned Westcott that supplied similar products, the acquisition was simply rolled into Westcott product line. A comparable corporate acquisition would have cost 1-3 times sales or 6-15 times earnings, so the savings were considerable.

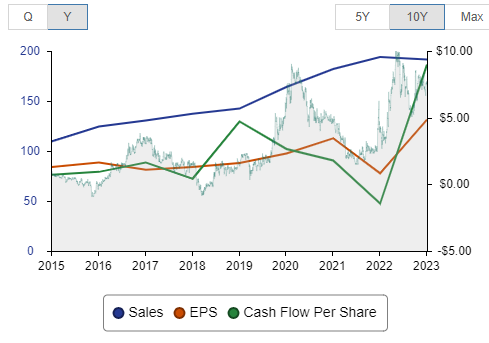

Income Statement

For the past 10 years, the company has grown its sales by a CAGR of 6% while the EPS has grown at 15.3% CAGR, which is very good.

The stock price has reflected this growth in business (the following chart is a 5 year plot of ACU stock price versus SPY, S&P 500 index ETF).

Today the company has a market value of $190 million and is a true small-cap stock. Its TTM revenues are $190 million (the market values the company at 1 times Sales), and a net income of $20 m which is equivalent to $5.06/share. At a stock price of $41.97/share as of Nov 15, 2024, it is currently trading at a price-to-earnings ratio of 8.29. The company currently pays a 1.4% dividend yield, with the dividend growing at 4.6% per year on average over the past 5 years.

The Company’s bank debt less cash as of September 30, 2024 was $26.7 million compared to $38.2 million as of September 30, 2023. During the twelve-month period ended September 30, 2024, the Company paid approximately $6.1 million for the acquisition of the assets of Elite First Aid Inc., distributed $2.2 million in dividends on its common stock, and generated approximately $6.2 million in free cash flow. Additionally, the Company realized net proceeds from the sale of the Camillus and Cuda product lines of approximately $13.0 million.

- Company Q3 quarterly report.

With the sale of Camillus and Cuda in 2023, the comparables next year are going to be impacted on the income statement as the revenue (and earnings) from these 2 lines will not be present. However, as you can see, the proceeds of approximately $13 million helped the company reduce net debt on the balance sheet by a similar amount.

Balance Sheet

From a long-term perspective, the balance sheet is trending in the right direction. In the last 10 years, the Assets have grown at a 7.7% CAGR, Liabilities have grown at a 4.1% CAGR and the stockholder’s Equity has grown at 10.6% CAGR. The company has become less leveraged.

The balance sheet today is strong. The Debt to Equity ratio is at 0.4, the current ratio is at 4.4 so the company is very liquid, and the interest coverage is at 12.6. In short, the company has ample liquidity to pay their employees and suppliers, as well as their lenders.

The stock today trades at 1.5 times book value and 2.1 times the tangible book value. They have $99 million in current assets and $59 million in total liabilities. It is not a net-net stock, but this shows that the balance sheet is very strong and at this time they have the ability to rebound from any minor hiccups or missteps.

Competitive Landscape

They are still a small company but they have been busy acquiring assets at good prices and growing responsibly. They have grown in their core shear category as well as added new adjacent categories like first aid and medical tools.

The following charts the company stock performance against the industry benchmarks

In the last 5 years, the stock has comfortably outperformed both the Consumer Defensive sector and the Household & Personal Products sector.

The companies chosen above serve a variety of markets, all overlapping Acme United’s markets in some way. A quick glance tells us that the valuation of ACU compared to the market peers is on the low side, more or less on every metric.

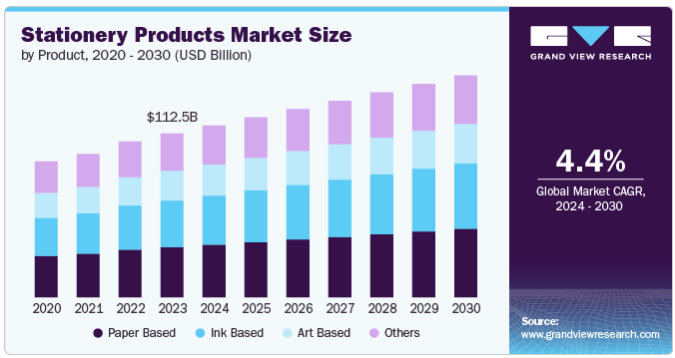

Both stationery products and first aid sectors are expected to grow in the coming years at a reasonable clip, close to 4-5% CAGR each.

There is always competitive jockeying for position in a growing market and it is hard to forecast the growth Acme United will experience, but given their history of incremental growth through disciplined acquisitions, and given their stellar balance sheet, it is reasonable to expect that they are likely to grow at rates faster than the market - meaning they will continue to gain market share.

Acme United Valuation Analysis, Estimate of Fair Value, and Our Buy/Avoid Rating

Given all the background and the context, and the understanding of their financial position and the market dynamics, it is now time to pull these all together into review of their current valuation, estimate of the fair price, our Buy/Avoid rating and profit potential if you were to buy the stock today.

Are you as excited as I am to discover if ACU 0.00%↑ can be your next double-digit winner? Let’s get to it then.